Understanding Subsidized vs Unsubsidized Loans: A Comprehensive Guide

For many individuals, deciding between subsidized and unsubsidized student loans can be a daunting task. The distinction between these two loan types affects not only your immediate finances but also your long-term financial health. This guide aims to simplify the differences, provide actionable advice, and equip you with the knowledge to make an informed decision that suits your financial circumstances.

The Problem and Solution: Navigating Your Loan Choices

The primary challenge lies in understanding the nuanced differences between subsidized and unsubsidized loans, especially regarding their repayment terms, interest rates, and financial aid implications. This guide will walk you through the intricacies of both types, offering insights into how each works and which might be the right fit for you. Whether you’re a prospective student or an experienced borrower, this guide provides step-by-step advice, practical solutions, and real-world examples to help you make the best financial decision.

Quick Reference

Quick Reference

- Immediate action item: Review your financial aid package to distinguish between subsidized and unsubsidized loans.

- Essential tip: Opt for subsidized loans to avoid interest accrual during your schooling.

- Common mistake to avoid: Forgoing the option of subsidized loans due to misconceptions about eligibility.

Detailed How-To: Understanding Subsidized Loans

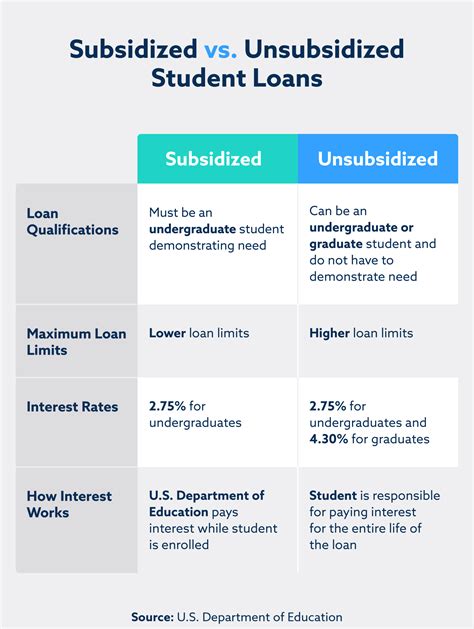

Subsidized loans are a type of federal student aid where the government pays the interest while you are in school, during grace periods, and during deferment/forbearance periods. This means you do not have to worry about interest accumulating while you’re studying, which can substantially reduce the overall cost of your loan.

To determine your eligibility for subsidized loans, your financial aid package will need to reflect that you meet certain criteria, such as financial need as determined by the FAFSA (Free Application for Federal Student Aid).

Step-by-Step Guidance

Here’s how to understand and take advantage of subsidized loans:

Determine Your Eligibility

To be eligible for a subsidized loan, you must complete a FAFSA and demonstrate financial need. Here’s a simplified breakdown of the process:

- Fill out the FAFSA form, ensuring all information is accurate and complete.

- Review the Expected Family Contribution (EFC) or Student Aid Index (SAI), which are calculated by the FAFSA. A lower number indicates greater financial need.

- Check your financial aid award letter for details on how much you’re eligible to receive in subsidized loans.

Review Your Financial Aid Package

Your financial aid package is a comprehensive document that includes details about the amount and type of aid you’re eligible to receive. Here’s what to look for:

- Ensure that your subsidized loan is included.

- Compare the total amount of subsidized loans versus unsubsidized loans.

- Look for details about the interest rate, repayment terms, and any conditions attached to the loan.

Understand the Terms and Conditions

Understanding the terms and conditions of subsidized loans can help you maximize their benefits. Here are some key points to keep in mind:

- Interest rates: As of 2023, the interest rate for subsidized loans is typically 2.75%.

- Repayment: No payments are required during school, grace periods, or deferment/forbearance.

- Grace period: After graduation, there is a 6-month grace period where no payments are required before the loan begins to accrue interest.

Detailed How-To: Understanding Unsubsidized Loans

Unsubsidized loans are another type of federal student aid, but in this case, the borrower is responsible for paying the interest that accrues while they are in school, during grace periods, and during deferment/forbearance periods. Unlike subsidized loans, there is no government payment of interest.

Step-by-Step Guidance

Here’s how to understand and navigate unsubsidized loans:

Determine Your Loan Eligibility

Unsubsidized loans are available to all eligible students, regardless of financial need. Here’s a breakdown of the process:

- Complete the FAFSA form, as this will determine your eligibility for financial aid, including unsubsidized loans.

- Review your financial aid award letter to see how much you’re eligible to receive in unsubsidized loans.

- Note that the interest rate for unsubsidized loans varies but tends to be slightly higher than subsidized loans.

Understand Interest Accrual

With unsubsidized loans, interest starts to accrue as soon as the loan is disbursed. Here’s how to manage this:

- Pay the interest as it accrues or consolidate it into the loan if you choose.

- Consider making interest-only payments during your schooling to manage the cost of interest.

Plan for Post-Graduation Repayment

Unlike subsidized loans, unsubsidized loans require payments after graduation:

- Review the loan terms carefully, which include repayment start dates, monthly payment amounts, and any grace periods.

- Make sure you understand grace periods and forbearance options to manage the transition from student loan recipient to borrower.

Practical FAQ

Can I convert my unsubsidized loans to subsidized loans?

Unfortunately, you cannot directly convert unsubsidized loans to subsidized loans. However, there are steps you can take to manage the differences:

- Consolidate your loans to combine the interest rates and create a single payment structure.

- Consider making extra payments during school to reduce the principal amount, thus reducing future interest.

- Explore refinancing options that may offer lower interest rates.

By taking these steps, you can effectively manage the financial burden of unsubsidized loans while optimizing your repayment strategy.

Conclusion

Understanding the differences between subsidized and unsubsidized loans is crucial for making informed financial decisions. By following this comprehensive guide, you’ll be well-equipped to choose the loan option that best suits your needs while avoiding common pitfalls. Whether you’re a current student or planning for the future, this guide provides practical advice and actionable steps to ensure you make the most of your financial aid.