When navigating the complex world of student loans, the decision between a subsidized and an unsubsidized loan can be particularly daunting. Understanding the nuances can make all the difference in managing your education finances effectively. This guide is designed to provide you with practical, step-by-step advice that will help you make an informed decision based on your specific financial situation. We’ll walk through the critical differences, common pitfalls to avoid, and real-world examples to clarify the options.

Understanding Subsidized vs Unsubsidized Loans

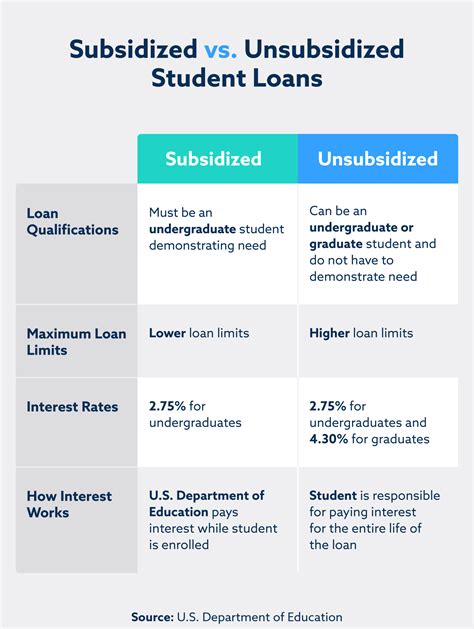

Student loans are a staple for many pursuing higher education, yet the terms and conditions can differ significantly between subsidized and unsubsidized loans. The primary distinction lies in how the interest rates are handled. With a subsidized loan, the government pays the interest that accrues while you're in school. For unsubsidized loans, however, you are responsible for paying the interest, whether or not you're enrolled at least half-time in an eligible program.

This guide will walk you through the critical components of both types of loans. We'll explore the immediate benefits, essential tips, common mistakes, and frequently asked questions to ensure you have all the tools needed to make a well-informed choice.

Quick Reference

Quick Reference

- Immediate action item: Calculate your Expected Family Contribution (EFC) or Federal Pell Grant award to determine if you qualify for a subsidized loan.

- Essential tip: Keep track of your school’s cost of attendance to maximize your loan benefits and avoid accruing unnecessary debt.

- Common mistake to avoid: Failing to understand the grace period and interest accrual for unsubsidized loans.

Choosing Subsidized Loans: The Pros and Cons

Subsidized loans can be an excellent financial tool if you meet the eligibility criteria. The government covers the interest, which can substantially reduce the amount of interest you pay over time. Here’s a detailed look at what you need to consider:

When applying for federal student aid, the government determines your eligibility for subsidized loans based on your financial situation. If you're accepted, you'll automatically receive a subsidized loan up to the amount your school certifies as needing to be covered by loans.

- Advantages:

- Interest is paid while in school, reducing overall debt.

- Based on financial need, reducing the risk of over-borrowing.

- Simpler application process since eligibility is determined by the school.

- Disadvantages:

- Only available to students who demonstrate financial need.

- Can limit the amount borrowed compared to unsubsidized loans.

- Limited to in-school borrowing; no interest subsidies on consolidation or refinanced loans.

Maximizing Subsidized Loan Benefits

To get the most out of your subsidized loan, follow these practical steps:

- Complete the Free Application for Federal Student Aid (FAFSA): This form determines your eligibility for federal student aid, including subsidized loans. Ensure you fill it out accurately and on time.

- Monitor your loan certification: Review the “Loan Settings” section on your FAFSA to ensure you're maximizing your subsidized loan eligibility.

- Stay on top of interest rates: Though the government pays the interest while you’re in school, it’s good to stay informed about the rates to understand the full picture.

- Keep track of the grace period: After you graduate, there's a 6-month grace period before you start making monthly payments. Use this time wisely to stabilize your finances.

By following these steps, you'll maximize the benefits of your subsidized loans while minimizing unnecessary debt.

The Ins and Outs of Unsubsidized Loans

Unsubsidized loans offer flexibility but require you to manage your interest payments. Let's delve into what to expect when you choose this route:

With unsubsidized loans, the interest accrues while you're in school, and you're responsible for paying it, although you can choose to set it aside or pay it off. This type of loan can be especially beneficial if you’re not eligible for subsidized loans or if you need to borrow more than what’s available under subsidized terms.

- Advantages:

- Available to all students, regardless of financial need.

- Can borrow up to your school’s cost of attendance (minus other aid).

- Offers greater borrowing flexibility.

- Disadvantages:

- Interest accrues while in school, which can add to your overall debt.

- Rates may be higher compared to subsidized loans.

- You’re responsible for all interest, even if you don’t pay it immediately.

Optimizing Unsubsidized Loan Use

To optimize your unsubsidized loan experience, consider these steps:

- Explore payment options: Decide whether to pay the interest while in school or let it accrue. If you choose to pay, it can help reduce your principal balance and overall interest.

- Keep meticulous records: Track all your loan details, including interest rates and accrued interest, to make informed decisions.

- Utilize grace periods and deferment options: Take advantage of the grace period after graduation to manage your debt before starting monthly payments.

- Refinance wisely: Look into refinancing your unsubsidized loans to potentially lower your interest rates and monthly payments.

Following these tips will help you manage your unsubsidized loans more effectively, reducing the long-term financial burden.

Practical FAQ

Can I convert a subsidized loan to an unsubsidized loan?

Unfortunately, you cannot convert a subsidized loan to an unsubsidized loan. Once you opt for an unsubsidized loan, you lose the government subsidy on interest. However, if you change your financial situation or drop below the required financial need level, you may become eligible for subsidized loans in subsequent years.

How do I know if I qualify for a subsidized loan?

To determine if you’re eligible for a subsidized loan, you must complete the Free Application for Federal Student Aid (FAFSA) and be deemed to have financial need based on the Expected Family Contribution (EFC) calculated from the FAFSA. Schools will determine how much of your need can be met with subsidized loans.

What happens to my unsubsidized loan interest while I’m in school?

The interest on your unsubsidized loan will continue to accrue while you’re in school, regardless of whether you pay it off or not. You have the option to pay the interest, which will reduce your principal balance, or let it accrue and pay it all at once after you graduate. Some lenders also offer an interest deferment option during school, although this depends on the lender.

This guide is designed to provide you with the practical knowledge and confidence to choose between subsidized and unsubsidized loans wisely. By understanding your options, following the best practices outlined, and asking the right questions, you can better manage your education finances and reduce your overall debt burden.