Understanding Your 75 Hourly Rate: Annual Earnings in 2023</h2> <p>Many individuals working in various industries find themselves negotiating or already earning an hourly rate of 75 in 2023. This substantial income can be a game-changer, but it’s essential to fully understand what this translates to on an annual basis, considering factors such as tax implications, benefits, and other financial obligations. This guide will walk you through everything you need to know to maximize your earnings and manage your finances effectively.

Problem-Solution Opening

If you’re earning $75 per hour, it’s natural to wonder just how much you can expect to make in a year. Given that, you might also be concerned about how taxes, deductions, and other variables impact your take-home pay. Our goal is to demystify these elements, ensuring you have a clear and actionable roadmap to maximize your annual earnings and financial well-being. Whether you’re considering this rate for a new job or managing your current finances better, this guide provides real-world examples, practical solutions, and expert tips to help you achieve your financial goals.

Quick Reference

- Calculate annual earnings with immediate action: Use a basic annual earnings calculator.

- Essential tip with step-by-step guidance: Factor in taxes and benefits.

- Common mistake to avoid with solution: Don’t forget about retirement contributions and savings.

Calculating Your Annual Earnings

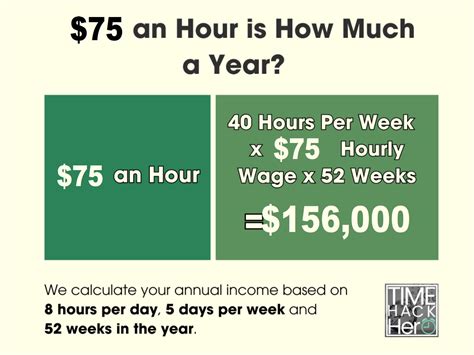

Let’s start with the basics: calculating your potential annual earnings at $75 per hour. To make this process straightforward, we’ll assume a full-time work schedule of 40 hours per week for 52 weeks a year.

Step-by-Step Calculation:

- Calculate weekly earnings: $75 x 40 hours = $3,000

- Calculate annual earnings before taxes: $3,000 x 52 weeks = $156,000

So, your potential annual earnings without factoring in taxes or benefits are $156,000.

Considering Taxes and Deductions

While the $156,000 is your gross income, your net income—what you take home—will be lower due to taxes and other deductions.

Understanding Federal and State Taxes:

The federal tax rate can vary based on your income and filing status, but a rough average for federal tax is about 25%. For state taxes, rates will vary by state. Here’s a simplified approach:

- Estimate federal taxes: $156,000 x 25% = $39,000

- Estimate state taxes (average rate around 5% for this example): $156,000 x 5% = $7,800

- Total estimated taxes: $39,000 + $7,800 = $46,800

- Net annual earnings: $156,000 - $46,800 = $109,200

This means your net annual income is roughly $109,200 after federal and state taxes.

Incorporating Benefits and Deductions

Besides taxes, other benefits and deductions can impact your take-home pay. These can include health insurance, retirement contributions, and other perks.

Step-by-Step Adjustment:

- Health Insurance: If your health insurance premiums are $1,000 per month: $1,000 x 12 = $12,000 annually

- Retirement Contributions: Assume a 10% contribution to a 401(k): $156,000 x 10% = $15,600

- Other Benefits: Any other deductions should be added similarly

- Total Deductions: $12,000 (health insurance) + $15,600 (401(k)) = $27,600

- Final Net Annual Earnings: $109,200 - $27,600 = $81,600

Maximizing Your Earnings and Benefits

Now that you have a clear understanding of your net income, let’s discuss how to maximize this amount. Here are actionable steps to ensure you’re not leaving money on the table.

1. Optimize Your Benefits Package:

- Review your benefits carefully. Opt for the most beneficial plans without over-committing to non-essential benefits.

- Consider flexible spending accounts for medical expenses if offered.

2. Maximize Retirement Contributions:

- Contribute as much as possible to your 401(k) or equivalent retirement plan to benefit from employer matches and tax advantages.

- Explore individual retirement accounts (IRAs) if additional contributions are possible.

3. Stay Tax-Efficient:

- Consider your tax bracket and strategize deductions. Large medical expenses, charitable donations, and mortgage interest are common tax-deductible areas.

- Consult with a tax professional to ensure you’re taking full advantage of all available deductions.

Practical FAQ

What are the best ways to invest my $75 hourly income for future financial security?

Investing is a critical component of financial security. Here are some actionable steps:

- Build an emergency fund: Start by saving 3-6 months’ worth of living expenses in a high-yield savings account.

- Invest in a diversified portfolio: Spread your investments across different asset classes, such as stocks, bonds, and mutual funds. Utilize target-date funds or robo-advisors for easier management.

- Utilize retirement accounts: As mentioned earlier, maximizing contributions to your 401(k) and IRA can yield significant long-term benefits.

- Consider real estate investments: If feasible, real estate can provide both rental income and appreciation over time.

- Consult a financial advisor: A professional can provide personalized advice tailored to your financial goals and risk tolerance.

Implementing these strategies will help ensure your earnings not only sustain you now but also grow and secure your financial future.

By thoroughly understanding your $75 hourly rate and its annual impact, you can make informed financial decisions that align with your goals. With these practical examples and expert tips, you’re better positioned to optimize your earnings and secure your financial well-being for years to come.